An Accountant's Guide to Understanding Lean Accounting

%20be%20truly%20invisible_.webp)

A few months ago, I worked with the finance team of a SaaS company during their month-end close. They spent nearly two weeks buried in spreadsheets, reconciling variances, chasing down allocations, and preparing long reports that no one in leadership actually used. By the time they finished, the close was late, the CFO was frustrated, and the numbers only created more confusion.

This isn’t unusual. Many accounting teams face the same problem. Traditional accounting creates too much noise: endless variance reports, complicated cost allocations, and data that comes in too late.

That’s where lean accounting comes in. In this guide, we’ll explore how it works, what makes it different, and how finance teams can use it to save time while creating real value.

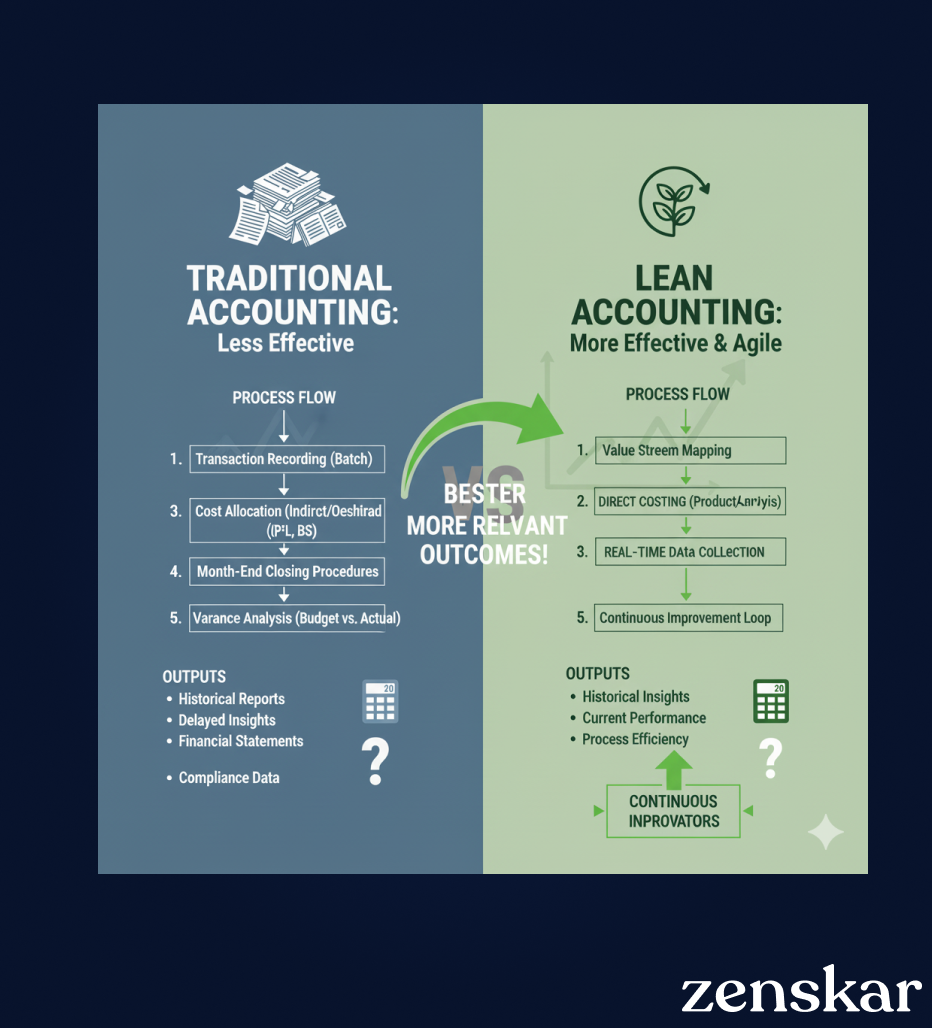

What is lean accounting?

The idea of lean accounting comes from lean business practices: cut out waste, streamline processes, and keep reporting simple and actionable. In accounting, the lean accounting philosophy means moving away from departmental cost tracking and focusing instead on value streams. A value stream is the complete set of activities a company performs to deliver a product or service to a customer, from start to finish. It focuses on tracking costs and performance by the work that creates real value, rather than by department.

What are the key characteristics of lean accounting?

Value stream costing

Instead of slicing expenses into dozens of cost centers, lean accounting groups them by value streams (product lines, services, or customer groups). This shows leaders which parts of the business actually create value.

Simplification

Reports are stripped of clutter. No endless variance schedules (detailed reports comparing budget vs. actual spending line by line), just clear numbers that highlight performance and problem areas.

Visual management

Data is presented in charts, scorecards, or dashboards so non-finance leaders can quickly spot trends without digging through spreadsheets. For teams that need to communicate these visual insights beyond internal dashboards, tools like the AI image generator can help finance and marketing teams quickly create compelling visuals and presentation-ready graphics that make data storytelling clearer for non-technical stakeholders.

Real-time reporting

Lean accounting pushes for faster closes and continuous reporting, giving decision-makers timely insights rather than backward-looking summaries.

Support for continuous improvement

Every report is designed to help identify waste, measure efficiency, and drive better processes, not just to check the box for compliance.

Investment in technology and processes

Lean accounting works only if companies are willing to invest in automation tools and streamlined workflows that remove manual bottlenecks. For example, using structured resources like an IT equipment inventory template can help organizations better track assets, reduce inefficiencies, and support more accurate financial reporting.

Cross-functional alignment

A harmonized connection between operations, finance, and the board ensures that feedback flows continuously and improvements stick.

What is the difference between traditional accounting and lean accounting?

When comparing traditional accounting vs lean accounting, the contrast is striking. Traditional methods were built for manufacturing-driven economies where efficiency meant controlling costs and variances. Lean accounting, on the other hand, is designed for organizations that move fast. As a result, many growing businesses combine lean accounting practices with outsourced accounting to streamline financial operations while maintaining accuracy and compliance.

What are the limitations of traditional accounting?

Traditional accounting creates a reporting burden that often hides, rather than clarifies, business performance. Its methods prioritize compliance and cost allocation, but they rarely provide actionable insights for management.

Variance analysis distorts performance

Standard costing and labor variances highlight efficiency gaps on paper, but they don’t show whether the business is improving customer value or reducing waste.

Example: A manufacturer hits its labor efficiency targets by producing larger batches, but excess inventory piles up in warehouses. The variance looks favorable, yet customer lead times actually increase.

Absorption costing hides profitability

Overhead allocations spread costs arbitrarily across products or services, making it hard to see which value streams truly generate profit.

Example: In a SaaS company, IT costs are allocated evenly across all products. The flagship enterprise product looks profitable, but in reality, its onboarding costs are so high that SMB contracts are the real profit drivers

Activity-based costing (ABC) adds complexity

ABC systems require extensive data collection, things like hours spent by employees on tasks, machine usage rates, support activities, and overhead drivers. All of this has to be tracked, categorized, and assigned to cost pools before costs can be allocated. The problem is that the level of detail rarely translates into decisions leaders can actually use.

Example: A services firm spent months logging consultant hours by task type, tracking travel time, and assigning shared overhead like IT support to projects. By the time the ABC report was complete, client needs had shifted and managers ignored the results, making the entire exercise feel like wasted effort.

Reports arrive too late to act

Financial statements and cost reports are produced weeks after period-end, reportedly leaving leadership with historical data instead of real-time guidance.

How can you implement lean accounting step by step?

Phase 1: Assessment and planning

- Review current processes like month-end close and reporting.

- Identify reports that take time but don’t help decision-making (for example, endless variance reports)

- Set clear goals: faster close, simpler reports, better alignment with business drivers.

- Involve finance, operations, and IT from the start to avoid silos.

Phase 2: Value stream mapping for finance

- Move from cost centers to value streams.

- A value stream is the full set of activities that deliver value to customers. In SaaS, a subscription value stream may include implementation, support, and engineering

- Value stream costing shows true profitability and highlights waste or bottlenecks.

Phase 3: Simplifying reporting systems

- Replace 50-page reports with clear, visual summaries.

- Focus on what leaders need most: revenue, margin, value stream performance.

- Use AI-powered analytics or one-page reports for speed and clarity. For example, show SaaS revenue by customer cohort or product line, instead of raw spreadsheets.

Phase 4: Training and change management

- Lean accounting is a mindset shift.

- Train accountants to think in terms of value streams, not just variances.

- Encourage cross-team collaboration with operations and product teams.

- Support continuous improvement with regular workshops and feedback.

Many organizations partner with accounting training providers to help finance teams adopt lean accounting effectively. For professionals in California looking to expand their tech skills alongside finance expertise, exploring IT training in California can provide complementary skills in automation, software tools, and data analysis. This ensures accountants focus on value creation and real-time insights rather than manual, low-impact reporting.

What essential features should lean accounting software have?

Choosing the right accounting software is critical for finance teams in scaling software companies. Modern lean accounting platforms must do more than bookkeeping, they should automate complex tasks, provide real-time insights, and support compliance. Key features include:

Automated revenue recognition (ASC 606 / IFRS 15)

Software revenue is rarely simple, subscription billing, usage-based pricing, and bundled contracts all add complexity. A lean platform should automate allocation, track performance obligations, and recognize revenue accurately under ASC 606/IFRS 15. This not only saves time but also eliminates the risk of misstatements and produces audit-ready schedules instantly.

Multi-entity and multi-currency support

As software companies expand globally, managing subsidiaries and intercompany transactions manually is unsustainable. A lean accounting system should consolidate financials across entities, support local GAAP adjustments, and handle real-time multi-entity transactions. This prevents reconciliation delays and ensures accurate consolidated reporting.

ERP, CRM, and payment integration

Accounting rarely operates in isolation. Integrations with ERP softwares, CRM, billing, and payment systems ensure that data flows automatically across the business.

Customizable dashboards and real-time analytics

Modern software should provide configurable dashboards with drill-down capabilities into revenue, cash flow, deferred revenue balances, and other KPIs. Real-time analytics allow CFOs and controllers to spot trends early and make proactive decisions instead of waiting for the month-end close.

Automated expense and procurement management

Vendor invoices, approvals, and procurement workflows can easily slow down operations if handled manually. Built-in automation for expense categorization, approvals, and payment scheduling streamlines the process, improves compliance with spend policies, and prevents delays in financial reporting.

How do top accounting platforms compare for lean accounting?

What are the common challenges in lean accounting implementation?

Overcoming the traditional accounting mindset

- Many finance teams are accustomed to detailed variance reports, departmental cost allocations, and long, historical-focused reporting. This makes shifting to value-stream-focused reporting feel unfamiliar and even risky.

- Actionable approach: Run hands-on workshops showing how simplified reports drive faster decision-making. Share examples of value stream metrics applied to real processes, like month-end close or multi-entity revenue recognition. Encourage accountants to experiment with visual dashboards before fully replacing old reports.

Technology and system integration issues

- Traditional ERPs often cannot support real-time value stream costing, multi-entity consolidations, or automated revenue recognition. Without integration, lean accounting reports risk being inaccurate or delayed.

- Actionable approach: Assess integration points before implementation, involve IT and operations early, and select an accounting software that supports automation, multi-entity, multi-currency, and real-time dashboards. Start with a pilot for critical processes to identify gaps and build confidence in new workflows.

How can you get started with lean accounting implementation with Zenskar?

Getting started with lean accounting doesn’t mean overhauling your finance stack overnight, it means introducing automation, clarity, and control where your team feels the most friction.

With Zenskar, finance teams can:

- Automate repetitive journal entries and revenue schedules so accountants spend less time on spreadsheets and more time reviewing insights.

- Recognize revenue in full compliance with ASC 606 / IFRS 15, even across complex SaaS bundles, usage-based contracts, or hybrid pricing models.

- Consolidate entities and currencies in real time, giving CFOs a single, accurate view of the business without waiting until month-end.

- Connect ERP, CRM, and billing systems seamlessly so source data flows into your GL without manual uploads.

- Provide audit-ready books and dashboards, ensuring transparency across every transaction, adjustment, and close process.

Book a free demo with Zenskar to experience how lean accounting can accelerate your close by 2x.

By automating recurring billing with Zenskar, our billing cycle – which previously took 7–9 days – now closes in 2 days, saving 16-20 hours/month.

Frequently asked questions

Lean accounting focuses on value streams, simplified reporting, and real-time metrics, whereas traditional accounting emphasizes departmental cost allocations, variance reports, and historical financial data.

Lean accounting applies lean principles to internal processes while maintaining GAAP-compliant financial reporting, ensuring that simplification does not compromise regulatory requirements.

Benefits include faster close cycles, clearer insights for decision-making, reduced manual work, and alignment of finance with operational improvements.

Implementation varies by company size and complexity, but most organizations see measurable improvements within 3–6 months when following a structured roadmap.

Lean accounting is ideal for scaling SaaS companies, mid-sized enterprises with complex revenue models, and organizations struggling with slow month-end closes or manual reporting. Finance teams dealing with multi-entity consolidations, usage-based billing, or ASC 606 compliance benefit most. Companies spending weeks on variance reports, cost allocations, and spreadsheets that don't drive decisions should adopt lean accounting to eliminate waste and focus on value streams.

Stay Future-Ready with AI-Native Order-to-Cash

Zenskar scales with you - it's flexible, reliable, and enterprise-ready.