How to Make Your Books Audit Ready and Organised in 2026

Audit readiness isn’t just about ticking boxes, it’s about protecting your financial integrity as you scale.

For growing businesses, staying audit ready means fewer surprises, lower costs, and faster audits. It shows stakeholders that your numbers are clean, your controls are strong, and your team is prepared to handle scrutiny. More importantly, it gives you year-round visibility and confidence, not just during audit season.

In this guide, we’ll show you how to keep your books audit ready in 2026 with fewer surprises, better systems, and year-round control. From internal processes to tech you actually need, we’ll break down what matters, what to avoid, and how to stay one step ahead, always.

What are the key benefits of maintaining audit-ready books?

1. Shorter audit cycles

Auditors don’t need to chase down missing entries or unclear transactions, which speeds up the process and reduces billable hours.

2. Fewer compliance headaches

With everything properly recorded and accounts reconciled, your risk of tax notices, penalties, or compliance flags goes down significantly. Using a compliance management platform can further help organizations monitor regulatory requirements and maintain audit readiness. If unresolved tax notices, audits, or liens are slowing term sheets or underwriting, specialized counsel can help businesses improve funding through tax solutions by negotiating resolutions, lifting liens, and packaging lender-ready compliance documentation.

3. Time saved during crunch periods

Instead of scrambling before audits or board reviews, your finance team can rely on clean records and shift focus to more strategic work.

4. Clearer visibility for leadership

Accurate books mean better insights into cash flow, margins, and runway, key metrics for CFOs, founders, and investors alike.

5. Greater trust from stakeholders

Whether it's your board, auditors, or future acquirers, audit-ready books signal that your company runs a tight, transparent operation.

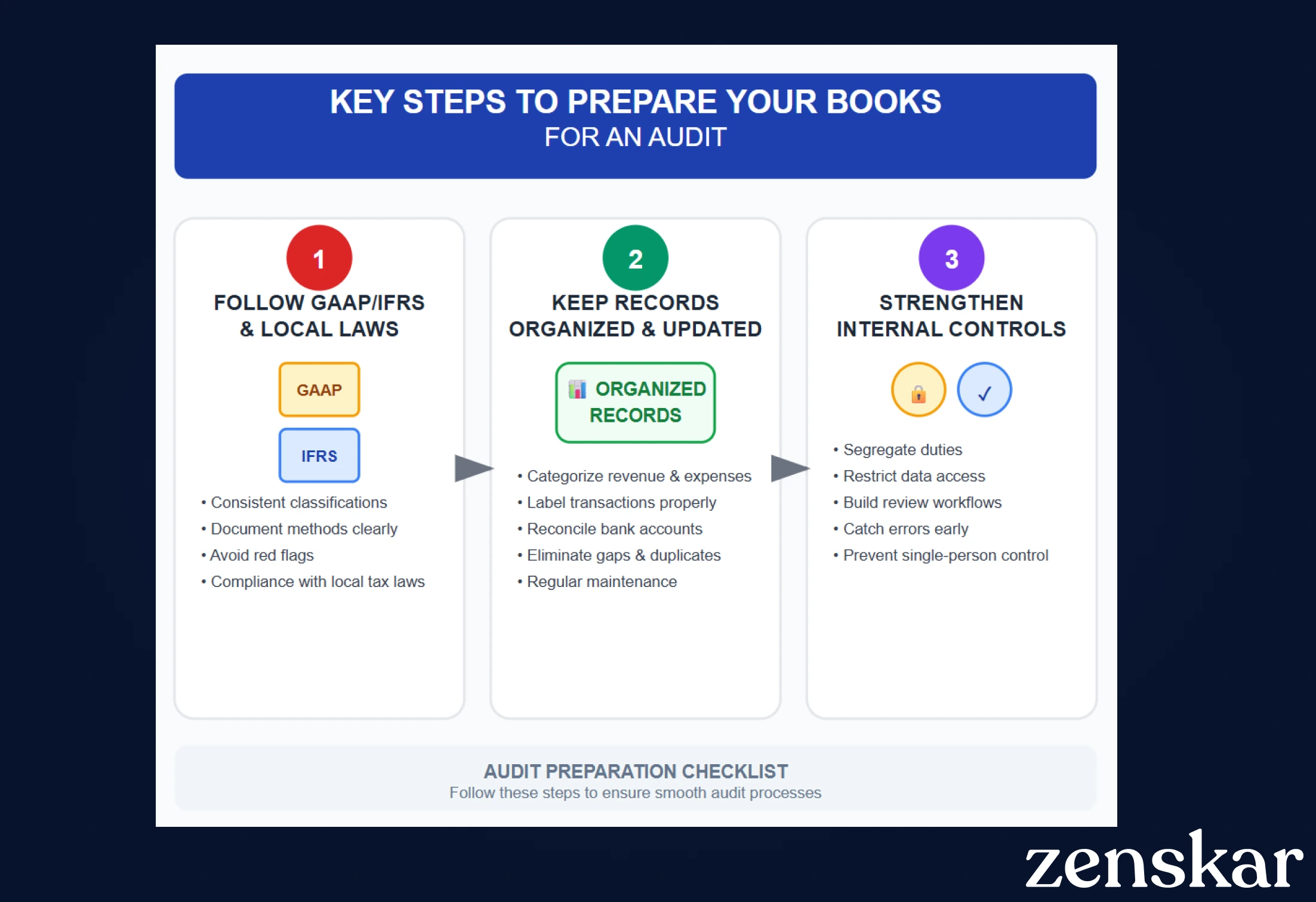

What are the key steps to prepare my books for an audit?

Preparing for audit isn’t about last-minute scrambling, it’s about building consistency, transparency, and control into your financial processes year-round. Whether you’re preparing for a routine audit or gearing up for due diligence, these steps will help you walk in confidently.

1. Follow GAAP/IFRS and local laws

Make sure your books follow GAAP and local tax laws. Even small deviations or inconsistent classifications can trigger red flags during audits.

2. Keep financial records up to date

Accuracy starts with organization. Regularly categorize revenue and expenses, label transactions properly, and reconcile bank and credit card accounts. Gaps, duplicates, or uncategorized entries slow everything down. If capacity is a constraint, hiring a virtual bookkeeper to own day-to-day categorization and reconciliation keeps your records clean without adding headcount.

3. Strengthen your internal controls

Internal controls are processes designed to catch mistakes, prevent fraud, and ensure the integrity of your financial data, before the auditor even steps in. One key principle here is segregation of duties: no single person should be responsible for handling, approving, and recording the same transaction.

Why? Because checks and balances reduce the risk of oversight or misuse. For example, if one team member is issuing payments, another should be responsible for reconciling them. Add review steps, restrict access where needed, and make sure every workflow has a second set of eyes.

What are the key pre-audit bookkeeping tasks?

Once your books are structurally sound, it’s time to zoom in on the finer details auditors will scrutinize.

Which financial reports should we review before an audit? [checklist]

1. Balance sheet

Double-check that all your assets, liabilities, and equity are correctly categorized and reflect the current financial position. General Ledger (GL) reports and trial balances should be accurate and in sync with your balance sheet figures. Ensure all adjusting entries are correctly passed and documented, with clear records of why they were made, who approved them, and supporting evidence for each.

2. Profit and loss statement

Make sure income and expenses are properly recorded in the right accounts and periods. Inconsistencies here raise red flags, especially around revenue recognition and expense allocation.

3. Cash flow statement

Auditors will expect to see a clear trail of cash inflows and outflows across operating, investing, and financing activities. This is where mismatches with other reports often show up, so run a quick reconciliation check.

4. Disclosures and Notes to Accounts

Disclosures provide context to the numbers and are essential for transparency. Review all footnotes and compliance-related disclosures to confirm they align with applicable accounting standards (e.g., Ind AS, IFRS, or US GAAP). Ensure key items like contingent liabilities, related party transactions, and accounting policies are accurately disclosed.

5. Inventory and asset verification

If your business holds inventory or fixed assets, ensure physical counts match your books. Check how depreciation, write-downs, and valuations have been recorded, it all needs to line up.

6. Account reconciliations

Reconcile all bank, credit card, and loan accounts. Any gaps between your general ledger and external statements should be resolved in advance, not during the audit, thereby making account reconciliations a necessity rather than an option.

Supporting reports

7. Trial balance

This serves as the base for your financial statements. All balances should be reviewed and tied back to the ledgers.

8. General ledger (GL) reports

These should be complete, reconciled, and support every line item in your statements.

9. Stock/Inventory reports

Ensure inventory counts are recent, reconciled with the books, and that valuation methods are consistent.

10. Payroll reports

Make sure salary expenses, provisions, and compliance with statutory requirements (e.g., PF, ESI, TDS) are well-documented and correctly recorded.

11. Adjusting entries summary

Maintain a clear, timestamped record of all journal entries passed post-closing. Indicate who approved them and the rationale behind each.

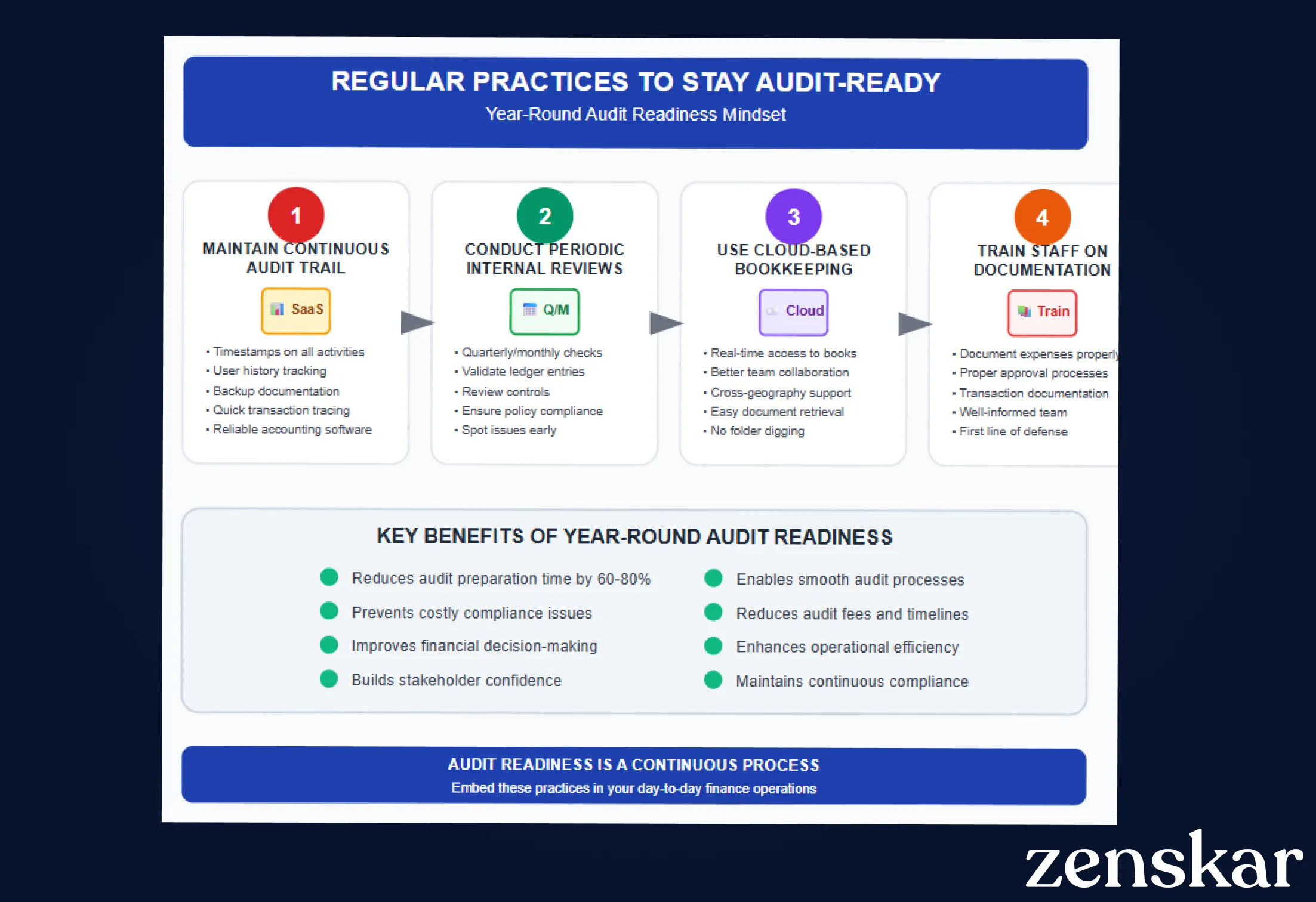

What are regular practices to stay audit-ready?

Audit readiness isn’t a once-a-year task, it’s a mindset that needs to be embedded in day-to-day finance operations. Here are five essential practices high-performing finance teams follow to stay audit-ready year-round:

1. Maintain a continuous audit trail

Use a reliable SaaS accounting software that logs every financial activity with proper timestamps, user history, and backup documentation. This helps trace transactions quickly, saving hours during audits.

2.Conduct periodic internal reviews

Run internal checks quarterly (or even monthly) to validate general ledger entries, review controls, and ensure compliance with financial policies. Spotting issues early prevents them from becoming audit problems later.

3. Use cloud-based bookkeeping systems

Cloud tools allow real-time access to books, supporting better collaboration across teams and geographies. They also make it easy to retrieve documents or reports requested by auditors, without digging through folders.

4. Train staff on documentation standards

Ensure everyone involved in finance knows how to document expenses, approvals, and transactions properly. A well-informed team is your first line of defense in an audit.

How can technology help streamline the audit process?

- AI-powered anomaly detection and real-time alerts: AI and machine learning tools like Microsoft Azure Anomaly Detector, Anodot, etc. can flag unusual transactions as they happen. For example, if a vendor payment exceeds typical monthly averages or an employee submits two identical expense claims, the system raises a real-time alert. These early warnings let finance teams investigate and fix issues immediately, reducing the risk of audit adjustments or compliance gaps later.

- Centralized cloud-based documentation: Cloud accounting and bookkeeping systems keep all your audit documents, receipts, contracts, journal entries, organized and easily accessible. Auditors get secure, permission-based access, reducing back-and-forth emails and speeding up the review process.

5 bookkeeping software to keep books audit-ready

Stay audit-ready year-round

Audit readiness isn’t just about recording expenses. It’s also about how companies are recognising revenue.

For enterprises with complex subscription-based or usage-based models, revenue recognition becomes a high-risk area during audits. Recognizing revenue correctly, whether it's time-bound or tied to performance obligations, isn’t something legacy bookkeeping software is designed to handle.

That’s why many finance teams pair their core bookkeeping tools with specialized RevRec software like Zenskar.

- Flexible revenue schedules: Create automatic deferred, unbilled, and unearned revenue schedules, and adjust without disrupting existing schedules.

- Multiple recognition methods: Set up straight-line, exact days, milestones, or usage-based approaches to match your revenue policies.

- Complete audit trail: Create journal entries with detailed timestamps. Review and post historical entries while maintaining intact locked periods.

- Multi-entity access: Manage separate ledgers for each legal entity and jurisdiction from a single login.

- Contract amendments: Recalculate revenue (future and past) for contract modifications with manual override options.

Maintaining a clean, auditable record of how revenue flows through your business is one of the smartest ways to stay audit-ready year-round.

If your revenue workflows add complexity to your audits, Zenskar can help. Take an interactive product tour or book a custom demo today to explore our RevRec offerings.

By automating recurring billing with Zenskar, our billing cycle – which previously took 7–9 days – now closes in 2 days, saving 16-20 hours/month.

Frequently asked questions

- Follow GAAP/IFRS and local laws strictly.

- Maintain an organized, up-to-date general ledger with accurate categorization and bank reconciliations.

- Automate journal entries with event-based accounting systems like Zenskar, which link entries to source documents for complete audit trails.

- Include approvals, rationale, timestamps, and ensure segregation of duties in recording and reviewing entries.

- Regularly reconcile ledger accounts to reduce errors and facilitate smooth audits.

- Cloud-based bookkeeping platforms (e.g., QuickBooks Online, Xero, Zoho Books) offer real-time reporting, audit trails, automated reconciliations.

- Specialized revenue recognition software like Zenskar enables flexible revenue schedules, multiple recognition methods, contract amendment tracking, and comprehensive audit trails.

- AI-powered anomaly detection tools provide real-time alerts on unusual transactions to catch issues early.

- Billing tools integrated with accounting (Zenskar) automatically generate compliant journal entries linked to invoices/contracts.

- Custom reports should include complete, reconciled trial balances, general ledger, adjusting entries summaries, and clear disclosure notes.

- Use cloud-based document management to store and share invoices, contracts, and audit docs securely for easy auditor access.

- Establish continuous audit trails with robust bookkeeping software.

- Conduct periodic internal review cycles to ensure controls and compliance.

- Train staff on documentation standards and approvals.

- Use automation for collections, billing, revenue recognition, and reporting to reduce manual errors.

- Keep clear documentation of related-party transactions and maintain transparency with stakeholders.

%20be%20truly%20invisible_.webp)

Stay Future-Ready with AI-Native Order-to-Cash

Zenskar scales with you - it's flexible, reliable, and enterprise-ready.