Recurring vs Reoccurring Revenue: When to Use Each?

.webp)

Every word in financial reporting has consequences.

Most founders, CFOs, and product leaders blur the line between recurring vs reoccurring revenue, and investors notice. In a pitch deck or a financial report, the difference may look semantic. But this could directly shape valuation, investor confidence, and audit scrutiny. Recurring revenue represents predictability and trust. Reoccurring revenue represents potential, but uncertainty.

The question worth asking is: Does your business truly have recurring revenue or are you dressing up reoccurring sales to appear predictable?

TL;DR

- Recurring revenue is contractual and predictable. It’s the income you can expect regularly at intervals, for example, monthly, quarterly, or annually.

- Recurring revenue is preferred by investors for its stability, visibility, and forecast accuracy.

- Think about Reoccurring revenue not like a contractual obligation, but as something that might repeat periodically (seasonal or event-based), with no fixed cadence.

- To avoid misleading metrics reoccurring revenue must be reported separately, even if it helps support early growth. Recurring revenue should follow deferred and scheduled recognition, while reoccurring is recognized upon delivery.

- Adopting consistent revenue reporting best practices ensures recurring and reoccurring streams are classified transparently for internal and external stakeholders.

- You need to use automated RevRec tools, such as Zenskar, which can help you consistently ensure a transparent, accurate separation between the two.

- For CFOs: codify renewal logic, keep reoccurring revenue out of ARR, and apply ASC 606 logic for automation and forecasting clarity.

What is recurring revenue, and why do investors prize it?

Imagine a company earning from contracts that renew in a predictable cycle. That is recurring revenue. For example, subscription, retainers, or service agreements. Their customers are hard-committing to paying periodically for services they value.

Today’s recurring revenue models are built on predictable renewals and automated logic that aligns financial reporting to customer contracts

The best example would be Netflix. Millions of subscribers every month renew without even thinking twice, a perfect example of contractual cash flow. The CFO can model forward 12 months of revenue with high confidence because the renewal logic is built into the customer relationship.

Now zoom into a SaaS scenario. Suppose your company has 200 customers paying $1,000 per month. That’s $200,000 in Monthly Recurring Revenue (MRR).

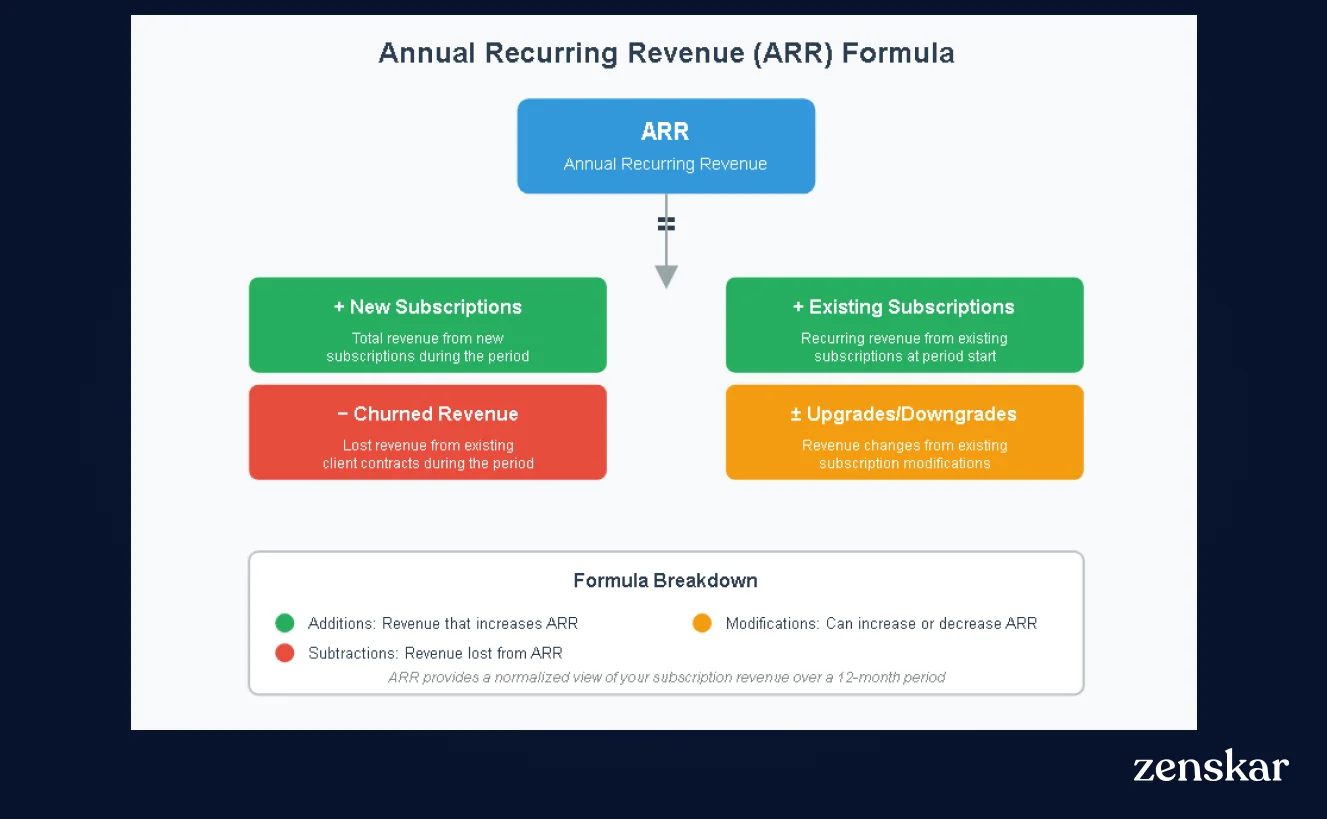

Annual Recurring Revenue (ARR) translates that predictable monthly income into an annualized view. But, a flat “MRR × 12” fails to capture mid-year churn, new bookings, and no upgrades, which makes this formula unrealistic in a dynamic subscription business.

Check out the formula below. This is how finance teams are often refining ARR even further to now include the actual movements of revenue across the year:

As an example, if your existing recurring revenue at the beginning of 2025 was $2 million, you added $600,000 in new recurring contracts, lost $100,000 in churn, and gained $200,000 in upgrades, your ARR for 2025 would be $2,700,000

$2,000,000 + $600,000 - $100,000 + $200,000 = $2,700,000

Whether your customers are expanding, contracting, or even leaving, this gives a clear and accurate view of how your recurring base evolves.

For multi-year contracts, ARR is typically annualized by dividing the total contract value by the number of years. A three-year $300,000 deal would add $100,000 to ARR for each active year of the term. When you get recurring revenue right, the capital tends to follow. Predictable, well-documented renewals turn your revenue base into something a lender or investor can underwrite with confidence, because they can see exactly what next year looks like before they commit a cent. That is why a clean ARR figure does more than impress a board deck. When your company is ready to scale, a strong and growing recurring base becomes leverage at the negotiating table, making it far easier to secure funding from external financing sources, from banks and equity investors who want to back businesses with cash flow they can actually forecast. In short, the more reliable your recurring revenue, the cheaper and faster your access to the money that fuels growth.

What is reoccurring revenue, and why is ‘repeat’ not ‘predictable’?

Reoccurring revenue is income that repeats, but without commitment. Customers aren't coming back because of a contract. They are doing so by choice.

Picture a marketing agency running campaigns for the same client every festive season. A D2C wellness brand where customers are reordering supplements based on need or even discount cycles, depends on reoccurring demand. Take a cloud infrastructure provider that sees usage spikes only when its clients launch new products. Appealing for sure in the short-term graphs, but there is a complete lack of foundation when it comes to predictability

From an accounting standpoint, reoccurring revenue cannot be recognized as contractual under ASC 606 because the performance obligation is not enforceable or time-bound. Unlike recurring revenue, which is recognized at specific points in time as contractual obligations are met, reoccurring revenue lacks enforceability and depends on customer choice rather than contractual commitment.

Investors treat it with caution because it reflects customer intent, not institutionalized retention. CFOs must resist the temptation to merge it with recurring metrics. Merging the two will often mimic stability and will eventually trigger painful corrections during due diligence.

Think of reoccurring revenue as the weather: you can forecast patterns but not the exact day it rains. Investors treat it as potential, not a financial guarantee.

Where do companies blur the line, and why is that risky?

The initial stage of growth is where these SaaS and service companies often blur the lines between recurring vs reoccurring revenue just to showcase momentum. The blurring often isn’t malicious. It’s just messy operations. But the market penalizes confusion.

Common pitfalls include:

- Setup fees can’t be recurring revenue: These fees are only collected once, so they should not inflate your recurring numbers.

- Seasonal clients are not your true recurring revenue: These clients do not have a term contract and therefore are not recurring.

- Usage-based spikes aren’t true MRR: Consumption that is variable can not be considered as contractual revenue.

This is why several SaaS firms have been facing valuation downgrades, because after investors reclassified inflated “recurring” metrics during their due diligence. These misclassifications often result in mandatory revenue reclassification and restatement when auditors scrutinize these classifications more closely.

The lesson: mislabeling revenue erodes trust faster than it inflates metrics.

What is the ultimate financial differentiator? Transparency.

Here’s where platforms like Zenskar step in. Zenskar automates compliance by embedding ASC 606 and IFRS 15 logic directly into every stage of billing and recognition.

Each contract is mapped to its performance obligations, deferrals are generated automatically, and revenue is recognized in real time with complete audit visibility, preventing misclassifications long before they reach the balance sheet. Zenskar’s AI analytics also let CFOs filter Net ARR by customer cohort, plan type, or region, turning raw billing data into insights that drive board-level reporting. As finance and SaaS teams adopt top AI platforms for revenue analytics, automation, and forecasting, they also need to validate how these systems handle changing billing data, usage spikes, and business-critical financial workflows before relying on them for operational and board-level decisions. To further reduce operational errors, many finance teams are also adopting robotic process automation to streamline repetitive billing and reporting tasks, ensuring greater accuracy and consistency in their workflows.

.webp)

When should you show reoccurring revenue?

Recurring revenue has been observed to form the foundation of enterprise valuation according to 409A valuation providers, but this doesn’t mean reoccurring revenue can't still play a vital role if reported transparently.

1. Early-stage startups

Companies in their infancy do rely heavily on reoccurring sales from a loyal customer base, all while testing pricing or value propositions. These early transactions can prove traction. However, CFOs must mark them down clearly as non-recurring, yet repeat income in their reports.

2. Usage-based and consumption models

Lately, adopting hybrid pricing charging based on API calls, transactions, or usage hours has been a go-to for many SaaS firms. Modern billing trends show a shift toward consumption-aligned pricing. Report rolling 90-day usage averages rather than pretending they’re fixed MRR. In these models, revenue is based on actual usage, but teams can maintain forward-looking visibility through rolling averages that serve as internal forecasting indicators.

3. Consulting and service firms

Agencies and implementation partners often get repeat projects from the same clients over time.

A meeting note taker can help document renewal discussions, client requests, and follow-up commitments from those conversations, making it easier to separate informal repeat interest from true contractual recurring revenue.

In the case of consulting and service firms, reoccurring revenue reflects the strength of those relationships, even without formal contracts. Tracking it separately helps teams gauge future pipeline potential more accurately.

Each case shows that transparency converts imperfection into credibility.

Lesser-known truths behind recurring vs reoccurring revenue

1. Renewal design is worth more than price

Automatic renewal with clear opt-out terms provides more valuation uplift than a manual renewal even at a 10% higher price. Predictability could beat nominal revenue growth.

2. Deferred revenue tells the truth

If you’re deferring revenue from a so-called “reoccurring” stream, you’ve likely embedded a pseudo-contract. Fix the contract or the logic before the auditors find it.

3. Cohort shape reveals fragility

A company with $10 million ARR across 200 customers can lose a $500,000 enterprise deal and see visible volatility. Investors now examine net ARR growth and ARR concentration to detect “fake stability.”

4. Repeat intent belongs to product, not finance

Reoccurring purchase data is gold for customer success and product teams but shouldn’t inflate ARR. It measures loyalty, not liability.

5. Automation is the quiet differentiator

Finance teams that automate classification and recognition gain a permanent credibility edge. Zenskar aligns billing cadence, ASC 606 rules, and revenue recognition schedules in real time. This continuous sync eliminates reconciliation gaps and gives CFOs a live view of financial performance accuracy.

The practical playbook for financial clarity

Building a recurring-revenue business or cleaning up your metrics demands structural clarity. Transparency is not just compliance; it is a competitive advantage.

- Define your metrics publicly: Document ARR, MRR, churn, and upgrade logic in every investor or board presentation.

- Separate ledgers: Keep different GL mappings for recurring vs reoccurring streams.

- Automate revenue recognition system: Use systems that apply ASC 606 performance obligations automatically and keep audit logs intact.

- Publish conversion roadmaps: If reoccurring demand is strong, share the plan to create contracts with retainers or prepaid bundles.

- Ensure easy audit trails: Zenskar automates classification and audit control at scale. Every transaction from contract creation to journal posting is traceable through a tamper-proof audit log. External auditors can verify recognition schedules and performance obligations directly in the system, reducing review cycles from days to minutes.

Zenskar enforces financial clarity by automating revenue-recognition logic, contract recognition, and unified reporting in one connected dashboard. It enables finance teams to visualize how different revenue streams (subscriptions, usage, overages) behave, allowing CFOs to demonstrate durability and transparency to boards and investors with confidence.

Book a demo or watch our product tour to discover how we're helping finance teams identify and report recurring revenue.

By automating recurring billing with Zenskar, our billing cycle – which previously took 7–9 days – now closes in 2 days, saving 16-20 hours/month.

Frequently asked questions

Recurring revenue is contractual and predictable; reoccurring is repeat business without obligation.

It lowers volatility, increases forecasting precision, and proves operational discipline, which are all signals of valuation stability.

It allows CFOs to plan liquidity coverage and investment cycles based on guaranteed inflows rather than expected ones. A strong recurring base also reduces the discount rate used in discounted cash flow (DCF) models, resulting in higher present valuation of future cash inflows.

Only after it becomes contractual or prepaid; otherwise, disclose it separately as “non-contractual repeat.”

Recurring contracts typically create deferral schedules while reoccurring income is recognized upon delivery with no deferral.

Stay Future-Ready with AI-Native Order-to-Cash

Zenskar scales with you - it's flexible, reliable, and enterprise-ready.